What makes the market truly interesting has never been only how much it rises today or falls tomorrow. Prices fluctuate, sentiment shifts, and themes rotate. But where capital ultimately flows is often far more worth watching than short-term market movements themselves.

Over the past period, whether it is global technology companies continuing to increase investment in artificial intelligence, or growing market attention on semiconductors, computing infrastructure, and commercial space, all point to the same fact: a new capital cycle is taking shape. Capital is no longer focused only on short-term narratives. It is paying increasing attention to who can represent future productivity, who can control foundational resources, and who can occupy a more important position in the restructuring of global industrial chains.

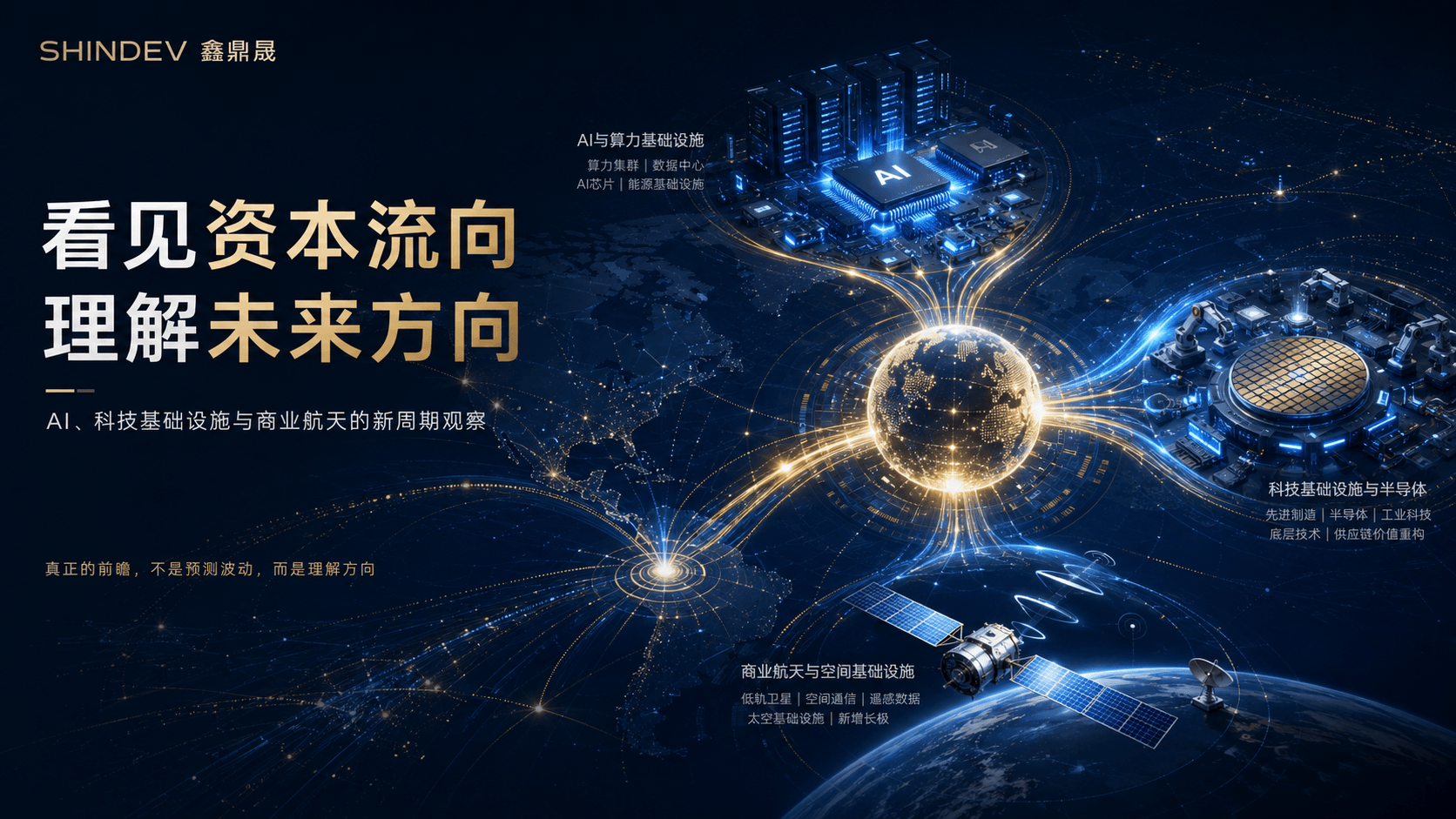

As of 2026, AI, technology infrastructure, and commercial space are no longer merely conceptual hotspots in the capital market. They have become measurable investment themes on a global scale. In its 2025 report Energy and AI, the International Energy Agency noted that global data center electricity demand is expected to more than double by 2030 compared with 2024, with AI-related data centers growing even faster. This means that AI competition is expanding from models and applications into deeper infrastructure layers, including computing power, energy, power systems, chips, cooling, networks, and data centers.

For SHINDEV, market observation is not simply about judging one round of market movement. It is about understanding where future value will be formed through capital flows, industrial change, and the global landscape. True foresight is not about chasing noise, but seeing direction before the noise emerges. It is not about staying at the conceptual level, but finding long-term value anchors through industrial chains, capital flows, and global resource allocation.

Today’s market may appear on the surface to be a rotation of technology themes, but at a deeper level, the global industrial structure is being reordered.

The rapid development of artificial intelligence has led the market to reassess the meaning of “technology.” In the past, technological innovation was more often reflected in improved product experiences or upgraded business models. Today, AI is entering enterprise operations, industrial production, financial analysis, medical research and development, content generation, automated decision-making, and intelligent manufacturing. It is gradually becoming a fundamental variable that affects efficiency, cost, and competitiveness.

This means AI is no longer only a matter for technology companies. It is a new efficiency revolution that the entire industrial system must face.

Recent market events also confirm this shift. In January 2025, OpenAI, SoftBank, Oracle, and MGX announced the launch of the “Stargate” artificial intelligence infrastructure project, with plans to invest up to USD 500 billion in AI data centers and related infrastructure in the United States. The significance of this project lies not only in its enormous scale, but also in the fact that it pushes AI competition directly into infrastructure competition: whoever can secure long-term computing power, stable energy, high-performance chips, and data center resources is more likely to gain the initiative in the next technology cycle.

The capital value of the technology sector is also changing. The market is no longer focused only on a company’s short-term performance. It is paying more attention to whether the company has key technologies, a position in the supply chain, infrastructure capabilities, and the ability to enter real industrial scenarios. Chips, computing power, data centers, advanced manufacturing, energy systems, industrial software, and new materials may seem like separate fields, but they are in fact jointly forming the foundation of future industrial competition.

The semiconductor industry provides direct evidence of this trend. NVIDIA’s fiscal 2026 revenue reached approximately USD 215.9 billion, with its data center business contributing about USD 193.7 billion, making it the company’s main growth driver. TSMC also achieved record performance in 2025 and announced that its 2026 capital expenditure is expected to reach USD 52 billion to USD 56 billion, with a focus on advanced process technologies, advanced packaging, and AI/HPC-related capacity. These figures show that capital is not staying at the AI application layer. It is moving at scale into foundational areas such as chips, packaging, computing power, and manufacturing capabilities.

Changes in the space industry are also worth noting. In the past, commercial space was more often seen as a high-investment, long-cycle field far removed from ordinary markets. But with the development of satellite internet, low Earth orbit communications, remote sensing data, commercial launch services, ground terminals, and space information services, space is gradually moving from a “national-level engineering project” toward industrialization, commercialization, and scale. It is no longer only a story about looking up at the stars. It has the potential to become an important component of next-generation communications, data, and space infrastructure.

Capital inflows into commercial space are also accelerating. According to Space Capital, global private investment related to the space economy reached USD 55.3 billion in 2025, up 65% from 2024. In the first quarter of 2026 alone, investment in the space economy reached USD 36 billion. Capital flows have shifted from early exploratory projects toward areas with stronger commercialization potential, including communications, remote sensing, navigation, defense resilience, and space data applications. At the same time, Starlink’s revenue reached approximately USD 11.4 billion in 2025, making it one of SpaceX’s most important revenue sources. This shows that low Earth orbit satellite internet has begun moving from technical validation into scaled commercialization.

From these developments, it is clear that the real direction of future markets is not the short-term rise of a single industry, but the recombination of new technologies, new infrastructure, and new industrial chains.

SHINDEV pays attention to these trends not because they are standing in the spotlight, but because they represent a deeper value logic: when technology begins to change production efficiency, when infrastructure begins to reshape industrial costs, and when global capital begins to reorganize around new industries, long-term opportunities start to emerge.

The most sensitive aspect of capital markets is that they often reflect the direction of the future in advance.

If in the past few years many funds were still chasing concepts, today more capital is beginning to concentrate in deeper, more solid, and more industrially certain directions. Especially in AI, technology, and space, the focus of capital is shifting from “who tells the best story” to “who truly owns resources, technology, and execution capability.”

AI is the clearest main theme.

As large model capabilities continue to improve, the market quickly realizes that AI competition does not only take place at the model layer. It also occurs across a more complete industrial chain involving computing power, chips, data, energy, networks, storage, cooling, operations, and application scenarios. Behind an AI application may be server clusters, high-performance chips, data centers, power systems, liquid cooling equipment, high-speed networks, and enterprise-level deployment capabilities.

This is why capital continues to focus on AI infrastructure. What truly supports the long-term development of AI is not a single application, but an entirely new digital foundation.

From the perspective of capital flows, the AI industrial chain has become increasingly clear across several layers: at the bottom are chips, computing power, and data centers; in the middle are large models, algorithm platforms, and developer tools; at the top are application scenarios such as enterprise services, smart terminals, robotics, autonomous driving, fintech, and industrial intelligence. Each layer may generate opportunities, but the density of value is not the same. The closer a company is to key resources and core capabilities, the more likely it is to build long-term barriers.

This is also what SHINDEV values more when observing the AI sector: not simply who stands at the center of public attention, but who occupies key nodes in the industrial chain; not only short-term popularity, but whether it has the ability to meet long-term demand.

The same is true for technology.

Global technology competition has entered a systemic stage. Semiconductors are not only about chips themselves; they involve design, manufacturing, packaging, equipment, materials, and application ecosystems. High-end manufacturing is not only about factory upgrades; behind it are automation, industrial software, robotics, sensors, and supply chain efficiency. Digital infrastructure is not only about building data centers; it is a comprehensive capability involving computing power, electricity, networks, security, and green energy.

Capital continues to enter these fields because they determine future industrial efficiency and a company’s position in global competition.

The space industry is becoming a new variable in technology capital observation.

With the accelerated development of low Earth orbit satellites, commercial launches, satellite communications, remote sensing data, and space information services, space is being redefined. It is no longer only a high-threshold scientific research project. It has the opportunity to become a new type of infrastructure serving communications, navigation, data collection, resource monitoring, urban governance, emergency management, and global connectivity.

For capital, the appeal of space lies in its industrial extensibility. Behind a satellite are not only manufacturing and launch, but also materials, electronics, chips, communications, ground equipment, data processing, AI analysis, application services, and long-term operations. It naturally has a long industrial chain, high technological density, and broad application potential.

More importantly, AI, technology, and space are not separate tracks. In the future, AI will need more data, and space can provide new data entry points. AI will need stronger computing power, and technology infrastructure will provide support. Space systems will require intelligent operations, while AI can improve their data processing and system management efficiency. A new industrial synergy is forming among the three.

This also explains why capital continues to move toward these directions. Capital is not simply chasing fashionable terms. It is searching for the new foundation of the future economy. Whoever can master key technologies, occupy core links in the industrial chain, and transform technical capabilities into real commercial value is more likely to be revalued in the new cycle.

For SHINDEV, capital observation is not about making judgments as soon as a hotspot appears. It is about asking further questions: Why is capital flowing here? Does this direction have long-term demand? Is the industrial chain deep enough? Can commercialization be realized? Is its position in the global landscape important?

Only by understanding these questions can market hotspots become more than short-term sentiment. They can become an entry point for understanding future value.

As capital flows into AI, technology, and space, another question becomes increasingly important: where can these capital, technology, and industrial resources be connected more efficiently?

Today’s global market is no longer a competition within a single market. Capital is moving across borders, industrial chains are being redistributed, technology companies are looking for more stable international platforms, and investment institutions are seeking regional hubs that are safer, more open, and more connected.

Against this backdrop, Singapore’s position as an international financial center has become even more prominent.

As an important international financial center in Asia, Singapore has long maintained a stable policy environment, mature regulatory system, open market mechanism, and highly international talent structure. It connects not only Southeast Asia, but also China, India, the Middle East, Europe, and the United States. It is not only an important hub for wealth management, asset management, and family offices, but is also continuously strengthening its role in green finance, the digital economy, fintech, and cross-border capital allocation.

Singapore’s role is also supported by real data. In the 39th edition of the Global Financial Centres Index released in March 2026, Singapore ranked fourth globally, behind only New York, London, and Hong Kong. At the same time, the number of family offices in Singapore has grown rapidly in recent years, with the number of single-family offices exceeding 2,000 by the end of 2024. The concentration of capital, family offices, asset management institutions, technology companies, and cross-border professional services in Singapore makes it not only a financial trading center, but also an important platform for capital allocation, technology investment, and industrial resource connection in Asia.

For global capital, Singapore’s value is not limited to the words “financial center.” Its value lies in its ability to serve as a stable, efficient, and trusted resource connection platform. At a time when global economic relationships are becoming more complex and industrial chain layouts more dispersed, capital increasingly needs a node that combines compliance, security, efficiency, and international connectivity.

This is why more and more companies and institutions are paying attention to Singapore. It is not only a channel for capital inflows and outflows, but also a platform for the recombination of technology, talent, markets, and industrial resources.

For SHINDEV, paying attention to Singapore is not simply about paying attention to one city. It is about focusing on the global allocation capabilities behind it. Future capital competition will not only be a competition of capital scale, but also a competition of resource integration capability, industrial understanding, and international coordination. Whoever can understand market changes from a global perspective and find connection points among different economic regions is more likely to capture long-term opportunities in the new cycle.

From AI to technology, from space to digital infrastructure, the new round of market opportunities is becoming more globalized and more industrialized. It is difficult to truly understand why capital flows by relying only on a local perspective. It is also difficult to determine which directions have long-term value by relying only on short-term market themes.

What SHINDEV aims to do is to see direction amid changes in the global market, understand industry through capital flows, and discover value amid industrial restructuring. Markets will rise and fall, and themes will rotate, but the directions that truly represent the future often become clearer through repeated capital choices, technological breakthroughs, and regional resource recombination.

The new capital cycle is no longer a simple industry rotation. It is a structural change jointly driven by AI, technology infrastructure, commercial space, advanced manufacturing, and global financial resources.

In the short term, markets will still be affected by interest rates, policies, geopolitical relationships, and risk appetite. But in the long term, capital will continue to seek directions that can represent future productivity, improve industrial efficiency, and form global competitiveness.

Therefore, the AI, technology, and space sectors that SHINDEV focuses on are not isolated market hotspots. They are part of a new cycle driven by real capital expenditure, industrial investment, corporate strategy, and regional resource allocation. AI infrastructure investment is increasing global demand for chips, computing power, energy, and data centers. Semiconductors and advanced manufacturing are becoming the foundation of technology competition. Commercial space is moving from high-threshold engineering toward the industrialization of communications, data, and space infrastructure.

SHINDEV believes that true market foresight is not about predicting tomorrow’s price, but about understanding the direction of the future. True capital value is not found in temporary popularity, but in continuously discovering, connecting, and amplifying value across key industries, key technologies, and key regions.

AI, technology, and space are becoming important coordinates in the new cycle. Global perspective, industrial understanding, and capital efficiency are the key capabilities for moving through cycles and capturing the future.

To see the direction of future markets, one must first see where capital is flowing. More importantly, one must understand why capital is flowing there.